ExxonMobil and Chevron delivered record-shattering profits last quarter, returns that financial news outlet Bloomberg described as ”almost comically huge.” Exxon, the world’s largest non-state energy company, posted $18.5 billion in profit, while Chevron, the nation’s second largest energy company, delivered $11.6 billion.

Even more notable is what oil companies are doing with their profits. Surprisingly, it may be very good news for climate change.

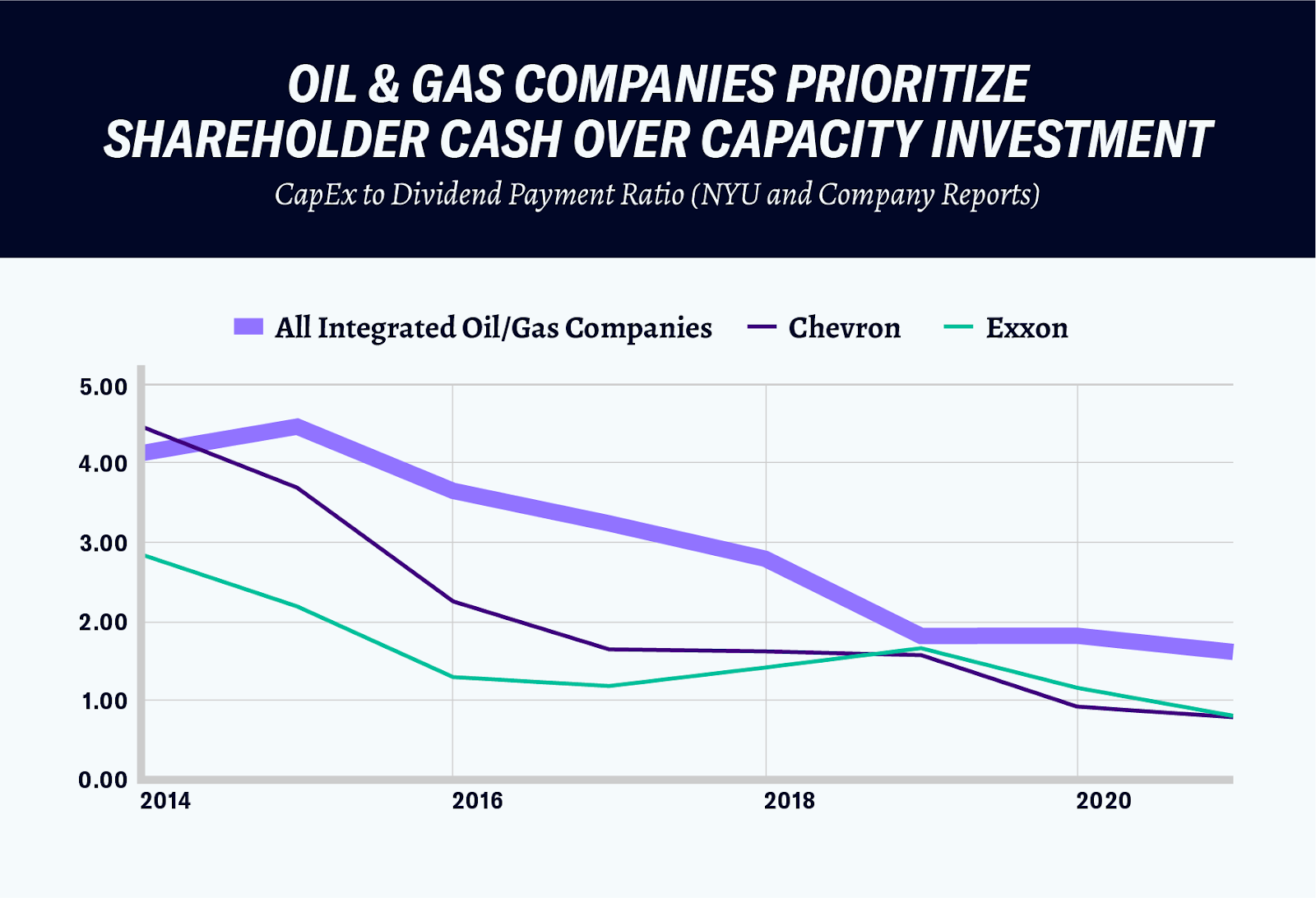

Broadly speaking, executives can use company profits in two ways. They can redistribute the profits to shareholders or reinvest the profits back into the business. In 2014, Chevron and Exxon reinvested over $68 billion through capital expenditures (CapEx). CapEx includes building new oil wells and repairing outdated refineries–both things that increase fossil fuel consumption.

This year America’s two oil giants are on pace to invest around $20 billion in CapEx—a decline of over 67% in less than a decade. Instead, management is focused on transferring as much profit as possible to shareholders. In Q2, rather than invest in future oil capacity, Chevron and Exxon showered investors with $6.7 billion in dividend payments and made promises of $30 billion worth of stock repurchases in the next few years. Right now the companies have already spent more on dividends than they did for all of 2014.

This development should be viewed as what it is: a market-based transition to clean energy.

Unlike the Green New Deal, which called for a “10-year mobilization” to transition the economy to renewable energy through a series of democratically-determined infrastructure investments, a market-based transition happens largely overnight and is divorced from accountability. Decisions on the future of America’s long term energy network are made by Wall Street and oil and gas executives.

The consequences were felt this summer. U.S. oil refineries operated above 90% capacity, but a lack of industry CapEx decreased the system’s overall capacity by about a million barrels a day compared to what it was pre-pandemic. Combined with Russia’s invasion of Ukraine, American oil companies couldn’t refine enough oil to meet demand. Gasoline rose to over $6 a gallon. Rising energy costs account for roughly half of the country’s inflation. Meanwhile, the industry booked record profits.

The Inflation Reduction Act, which President Biden signed into law this week, attempts to mitigate some of the worst impulses of a market-based transition. It provides subsidies to make clean energy cheaper, while making it more expensive to extract oil from federal lands. If fossil fuel extraction is less profitable, the theory goes, investment in it will go down.

Energy firms may be willing partners in this trend. In 2014 major oil companies invested about $4 back into their businesses through CapEx for every $1 they paid out in dividends. Today they invest just $1.67 for every dollar spent on dividends. Chevron and Exxon invest even less–under one dollar for every dollar of dividends. Contrary to what American oil executives say, the lack of investment isn’t caused by Joe Biden or Democratic posturing. It’s a transition nearly a decade in the making. In Trump’s first year of office, Exxon invested less than 50% of what it did during the Obama presidency.

Proponents of the oil and gas industry seem to confirm the market transition in their public comments. “I personally don’t believe there will be a new petroleum refinery ever built in this country again,” Chevron’s CEO Michael Wirth told investors at a conference in June. Why invest billions of dollars over ten years when more and more consumers and governments are demanding a transition? Instead, executives are opting to transfer millions to shareholders.

In a later interview, Wirth suggested that high oil prices are here to stay. An analyst paraphrased his view during the Q2 earnings call: “Any weakness in oil prices is going to be fleeting because of the under investment.”

American oil and gas infrastructure is deteriorating, and the oil and gas companies have shown little interest in maintaining it.

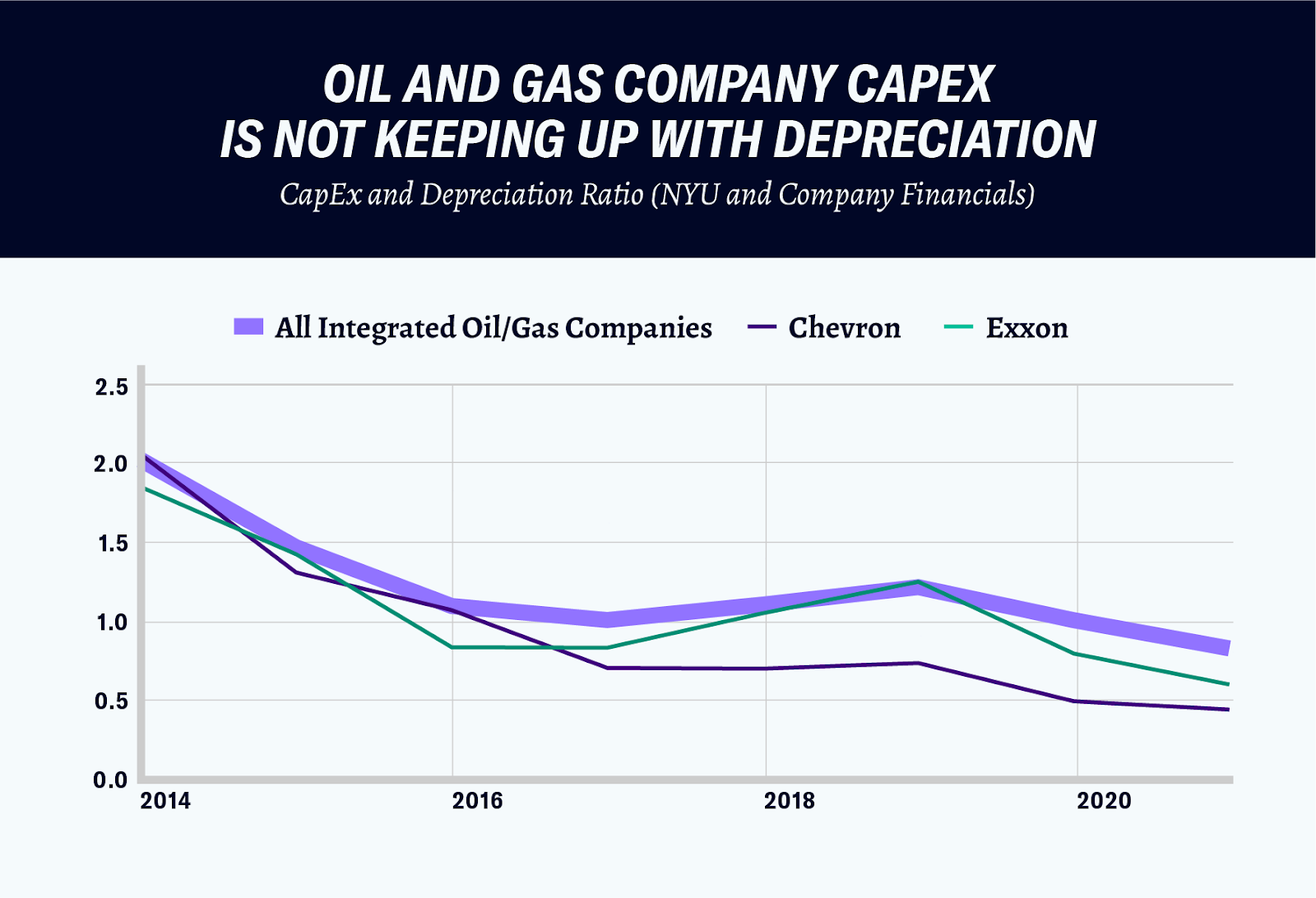

- A CapEx / Depreciation ratio can be used to evaluate if a company is making enough long term investments in its infrastructure. Roughly speaking, a ratio less than one means a company’s physical assets are depreciating quicker than management is replacing them.

- In 2021, according to data from NYU, the ratio for the 46 public firms that make up the integrated oil and gas industry dropped below 1 to .85, the first time in recent memory. Integrated companies handle upstream (discovery and production) and downstream (refinery, transportation, marketing) aspects of energy.

- Exxon’s CapEx / Depreciation ratio has been below the 1 threshold for 4 of the last 6 years. Chevron was below for 5 of the last 6 years, including bottoming out at .46 in 2021.

- Oil and gas companies have embraced automation and layoffs, resulting in lower operating costs across the sector. The industry has shed almost 50,000 workers since 2014.

American oil and gas companies are not making meaningful investments in clean energy.

- According to Bloomberg, investment by oil and gas producers in clean energy totaled $12.7 billion in 2020. European companies led the charge, with the “bulk” of those investments coming from Shell, Total, Repsol and Galp.

- Relative to dividend payments, American energy giants’ investments in environmental mitigation and clean energy are declining. In 2013, Exxon and Chevron spent 55 and 36 cents on environmental expenditures for every $1 they paid in dividends. In 2021, the ratio dropped to just 31 and 19 cents.

- Last year Exxon made headlines when an activist investor pushed the company to quadruple its annual spending on low-carbon energy to $3 billion a year. Despite the significant increase, it was almost $18 billion less than the company spent on dividends and stock repurchases in the last 12 months.

The Inflation Reduction Act will temper the negative impacts of a market based transition and lower costs for consumers

- The law provides $369 billion to combat climate change through a mixture of direct spending and tax incentives.

- It provides tax credits for consumer purchases and industrial production of renewable energy.

- Analysts predict it will reduce net emissions by 31%-44% below 2005 levels, while delivering cost savings. The average residential electricity bill is expected to decline by between $730 and $1,135.

- It mandates auctioning millions of federal acres for oil and gas development. If recent history is a guide, the auctions may end up being immaterial to America’s fossil fuel use. If enacted, the royalty rate companies must pay the government would increase 33-50%. According to an oil industry interest group, “That would make investing in these tracts less attractive.”

- The fossil fuel auctions are tied to renewable energy projects. The arrangement may needlessly complicate and delay viable renewable investments, as new fossil fuel infrastructure projects become a riskier bet for oil and gas companies.

The transition from fossil fuels is happening. It’s just a question of how painful it will be for average people. This year answered the question of what a market transition looks like: It hurts. War, limited alternatives, and decreased capacity combined to generate less emissions than before the pandemic at record prices for consumers. The prices translated to “comically huge” profits for oil and gas companies.

Without any government intervention, that’s the clean energy transition we’re headed for.