Supermarket chain Kroger used acquisitions to become the nation’s second-largest grocer. Now, flush with cash from record-breaking profits throughout the pandemic, management is looking to buy rival Albertsons for nearly $25 billion. If approved, the merger will create a $210 billion grocery titan. The deal raises major questions from shareholders, workers, and regulators.

Kroger currently operates 2,800 stores across 35 states and controls nearly 10% of the U.S. grocery market. Albertsons owns 2,273 stores, primarily on the west coast, and represents 5.7% of all grocery sales. According to data from Numerator, the combined company would control almost 16% of the national market.

- Kroger reported an operating profit of $3.7 billion in the last fiscal year—an increase of 39% from pre-pandemic times. Albertsons operating profit rose 70% during the same period.

The deal is sure to attract significant criticism from antitrust enforcers. “This merger is a cut-and-dry case of monopoly power,” Sarah Miller, executive director of the American Economic Liberties Project, told the Financial Times. “Enforcers should block it.”

The Biden administration has paid significant attention to antitrust, arguing that corporate concentration is a driver of several economic woes—including inflation. Last summer President Biden issued an executive order with 72 directives that pushed federal agencies to “vigorously enforce antitrust laws” and promote competition.

- The grocery industry evolved regionally, making national sales stats somewhat misleading. At 20% of all sales, Walmart is the nation’s largest grocer. 20% may not seem like a lot, but Walmart captures more than 50 percent of all grocery sales in 43 different U.S. metro areas, including 83% in Bismarck, N.D. (pop. 135k) and 60% in Oklahoma City (pop. 1.4 million).

- Kroger and Albertsons have significant geographic overlap in several major metropolitan areas. The new Kroger would exert considerable control over the Seattle, Los Angeles, San Diego, and Houston markets. “This is where the concern comes,” equity researcher Jen Bartashus told Bloomberg Radio. “The FTC has become increasingly critical of big mergers and may really push back.”

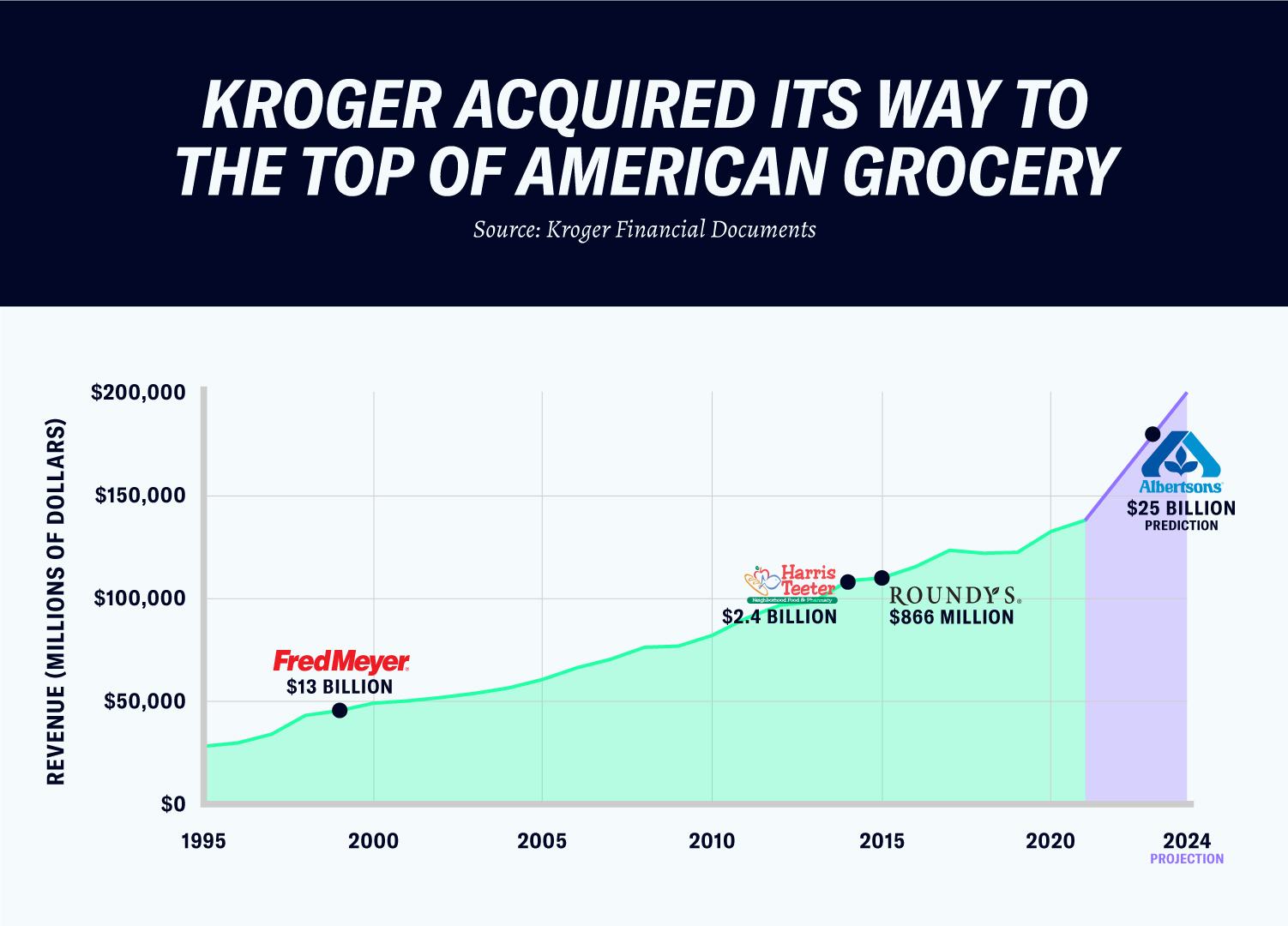

Since the decline of antitrust enforcement in the late 1970s, the grocery industry entered a period of mass consolidation. During one six month span, roughly 10% of the American grocery market merged. Kroger has been one of the most aggressive acquirers—expanding its footprint from the Midwest to both coasts.

- In 1998, Kroger announced it acquired Fred Meyer, then the nation’s fifth-largest grocer, for $13 billion. A year later the deal closed, and the company added 800 West oast stores to its footprint.

- In 2014, Kroger purchased Harris Teeter for $2.4 billion. The acquisition added 212 stores throughout the mid-Atlantic.

- In 2015, Kroger entered the Wisconsin market by acquiring Roundy’s for $866m.

According to management, the business rationale for each deal is straightforward. A bigger Kroger will have greater bargaining power against suppliers, allowing the company to negotiate better prices and pass savings on to consumers. Increased buying power also allows the company to command additional promotional price discounts from manufacturers–which could expand margins. All together, they’re betting that a combined company can streamline operations and generate greater synergies (cost cuts).

Kroger management promised investors cost synergies of $1 billion a year for the Albertsons acquisition. Management also committed to investing $500 million into lower prices for consumers and providing $1 billion for raises across the joint organization. Follow through on those commitments is uncertain.

- Research from the FTC found that grocery mergers in concentrated markets resulted in consumer price increases.

- Synergies for corporate mergers are overstated. Most mergers fail. “Study after study,” management icon Clayton Christensen wrote in Harvard Business Review, “puts the failure rate of mergers and acquisitions somewhere between 70% and 90%.”

- A 2020 internal document revealed that 1 in 5 Kroger associates are on food stamps.

So far, Wall Street is not buying the merger’s rationale or Kroger’s assurances of lower prices. Kroger’s stock is down nearly 10%, while Albertsons is off 7%. Most analysts are skeptical that the FTC will allow the merger. In an investment note, a Morgan Stanley analyst argued that historically large grocery mergers are not a guarantee for a more profitable company, but times may have changed. “Perhaps the industry has reached a point of consolidation such that a potential merger of this magnitude could result in structurally higher margins,” the analyst wrote. “The industry may be closer to oligopoly than we think.”

One big winner in the transaction is Cerberus Capital Management. The New York based private equity firm has owned parts of Albertsons since the mid-2000s. “It’s pretty clear,” Food Trade News reported, “to most observers that Cerberus wants out.” Cerberus currently controls 30% of the company and is poised to earn up to $7.1 billion from the sale. They aren’t the only winners. If the transaction is completed, Albertsons CEO Vivek Sankaran is in line for a $50 million payout.

Sankaran joined the company in 2019.