By Eric Gardner

Company data from Tyson Foods indicates that the meat processing giant used its size and power to extract an additional $500 million from American consumers last quarter under the cover of inflation.

Both the Biden administration and a broad swath of economists have accused Tyson of using its dominant market power to dramatically inflate meat prices at the expense of consumers and ranchers. The company’s latest earnings report backs up these charges and gives an indication of how much revenue Tyson may be generating through price gouging.

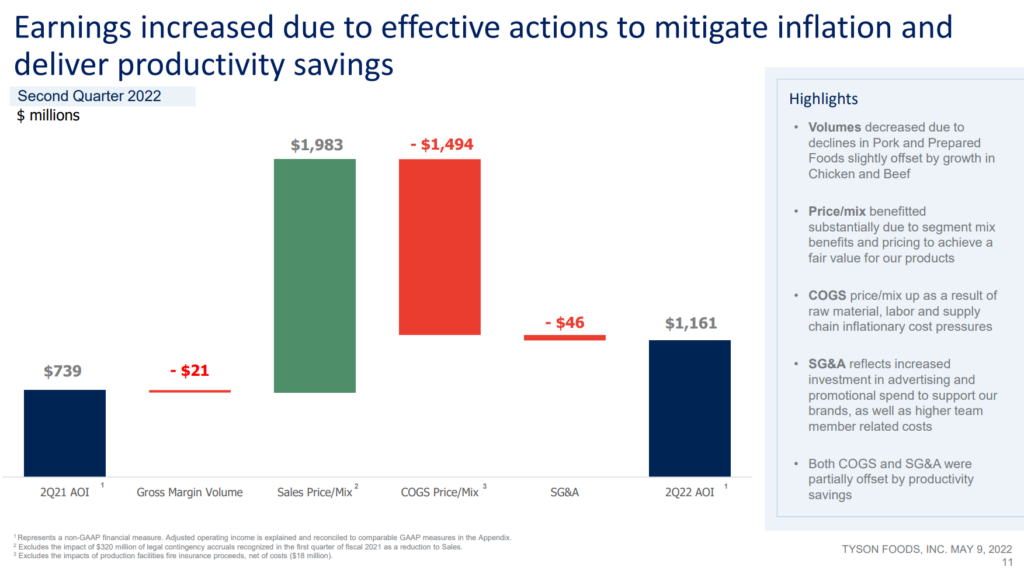

In the second quarter of 2022, the Arkansas-based conglomerate estimated that it responded to roughly $1.5 billion in higher costs with almost $2 billion in corresponding price increases. That difference is potentially half a billion dollars paid directly out of consumers’ pockets.

Tyson Foods’ quarter was one of the most profitable in recent memory. The company earned $1.2 billion on $13 billion worth of sales, while expanding its operating margin by 38% from the same quarter last year, generating more profit on every dollar of sales than it has in any second quarter in over a decade.

Critically, Tyson’s profits were delivered despite the company lacking significant brand power that’s typically associated with premium pricing. Companies like P&G, Coca-Cola and Clorox spend billions of dollars each year establishing premium brands in order to command higher prices from consumers. But according to Wall Street research firm Morningstar, approximately 80% of Tyson’s products lack significant brand equity and are considered “undifferentiated” or “commoditized.”

In a competitive market, Tyson would struggle to raise prices for largely undifferentiated products, let alone pass on inflation to consumers. Instead, it would need to absorb additional costs and keep prices low to risk a competitor gaining market share by undercutting them on price.

However, what Tyson lacks in brand equity, it makes up for in raw market power. With $47 billion in annual revenue, Tyson Foods is the number one beef and chicken processor in America and one of four firms that dominate America’s meat processing industry.

To put the company’s size in perspective, if Tyson was broken up into its individual operating units, the beef business ($18B) would rival grain giant General Mills ($17.6B) and the chicken business ($13.7B) would still be $2 billion larger than rival meat packer Hormel ($11.4B). The Prepared Foods group ($8.9B) would eclipse JM Smucker ($8.0B). Pork, the smallest American business unit ($6.3B), would equal spice monopolist McCormick ($6.3B).

In modern America, retailers (supermarkets, for example) typically exert a high level of control over manufacturers. The consolidation of big retail chains enables retailers to demand lower prices during negotiations, often accounting for 20% of a manufacturer’s total revenue.

But meat may be the exception. Research from the Food Marketing Institute shows that meat is the primary driver of consumer grocery store choice. Tyson’s massive size enables it to consistently pass supply chain costs on to retailers, who have few options. Retailers then ultimately pass the cost onto consumers – despite selling largely undifferentiated products. “We’re not asking them to pay for any inefficiency that we have,” Tyson’s CEO claimed at a recent industry conference. “We’re just asking you to pay for the inflation.”

But Tyson’s earnings report suggests that’s false. In fact, Tyson wants consumers to pay for inflation plus up to $500 million more. And consumers don’t have much of a choice because Tyson has the market power.

“We’re really positioned in a place where, from an elasticity perspective, we’re going to capture the consumer,” CFO Stewart Glendinning told the same industry crowd, referring to the concept of a consumer’s willingness to pay higher prices. “It’s just a question of where in the portfolio they’re going to go.”